A Lifestyle Spending Account (LSA) is a flexible account that helps you live your healthiest life. You can use the money in this account to buy a variety of lifestyle and wellness products and services. Continue reading to learn all about how a LSA works.

What you need to know

-

Your employer decides what expenses are covered

-

It’s considered a taxable benefit

-

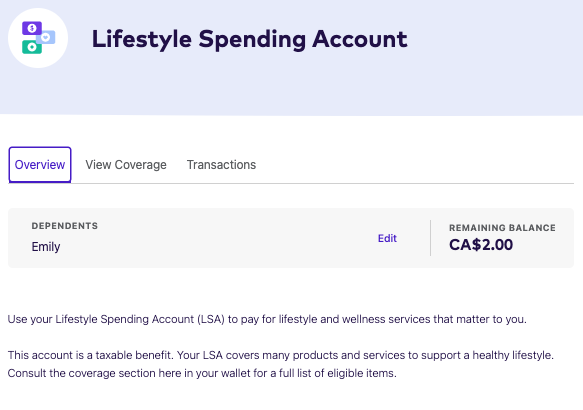

Your dependents can use the money too!

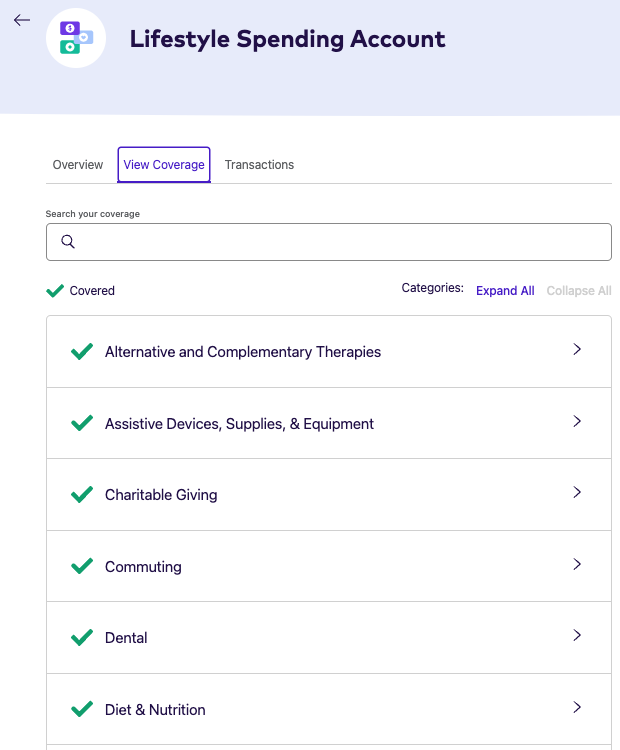

Find out what’s covered

LSAs can cover a huge variety of products and services. Some examples of categories that might be covered are:

-

Fitness (like gym memberships)

-

Pet products & services (like vet bills)

-

Vacationing (like plane tickets)

Keep in mind these are just examples. Your benefits plan is unique, and your employer decides what categories and items are covered. An entire category may not be covered, or some expenses within a category won’t be covered while others are.

Learn more about what’s covered by your LSA.

It’s different than a Health Spending Account (HSA)

There are two main differences between a LSA and an HSA:

-

Money in a LSA can be spent on a variety of wellness products and services, while an HSA can only be used for things that are considered medically necessary by the CRA.

-

Money spent from a LSA is considered taxable, while money spent from an HSA isn’t taxed (with the exception of Quebec).

Understand how you’ll be taxed

LSAs are considered a taxable benefit. What does this mean? You’ll be taxed on any money you spend from this account because it’s considered additional income. This tax is usually removed from your paycheque. If not, your employer will provide you with a T4A form to include when you file your taxes.

Some things to keep in mind:

-

Money you spend from your LSA will be taxed based on your marginal income tax rate.

-

If the tax is taken from your paycheque, your employer decides how often this happens. For example, they may tax you at the end of each quarter for any LSA money you spent during that quarter.

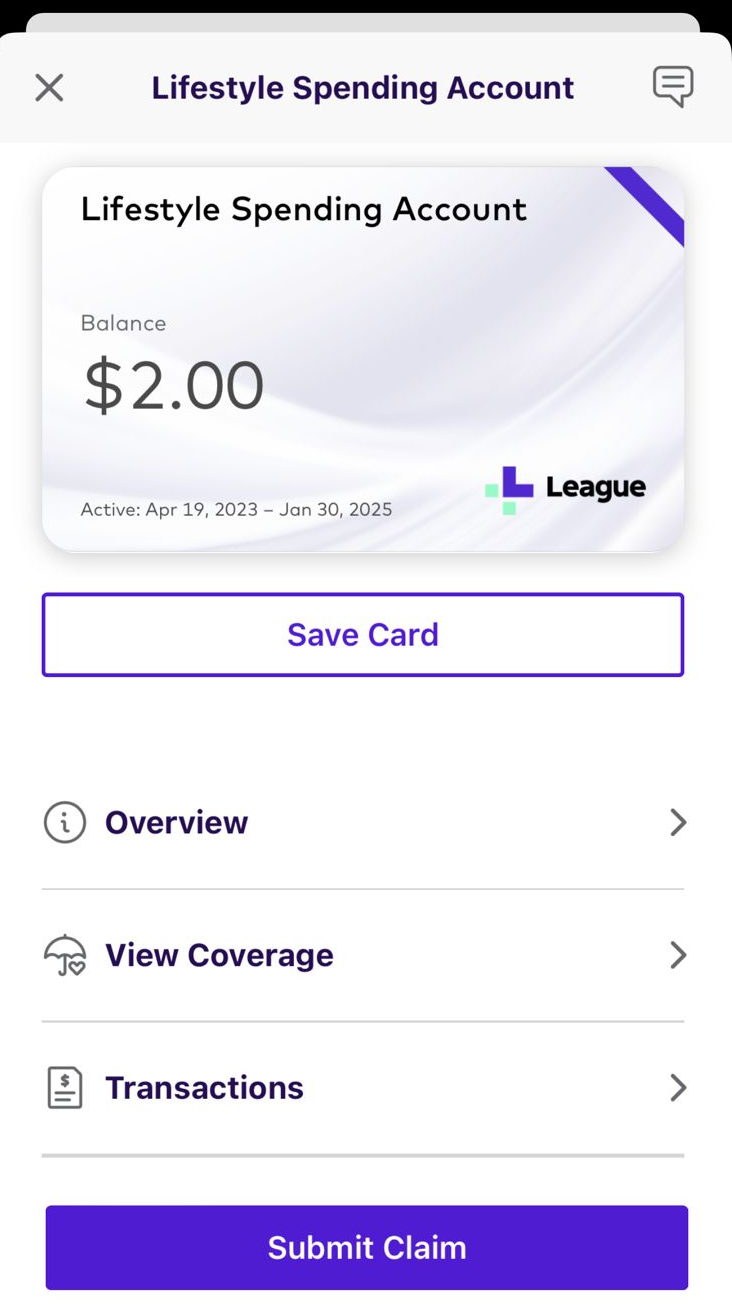

Submit claims

To spend the money in your LSA, make a purchase and submit a picture of the receipt and any other required information in your League Wallet.

Some things to remember:

-

You can only use your LSA to reimburse money you’ve already spent.

-

Before submitting a claim to your LSA, check if the expense is also covered by your benefits plan. If it is, you should always submit the claim to your carrier first!

-

Claims must be for eligible expenses that you paid for after your benefits became active (if you’re a new hire) or during your current plan year (if you’re an existing employee). For example, if your new plan year started in 2020 and you got new money in your LSA, you can’t use this new money to cover 2019 expenses.

Coordinate your benefits

If an expense is covered by both your benefits plan and your LSA, it should always be submitted to your benefits plan for reimbursement first. If your benefits plan doesn’t cover the full amount, you can then submit the remaining balance to your LSA. This is known as Coordination of Benefits (COB).

Tip: Learn more about COB.

Spend on your dependents

You can also spend the money in your LSA on your dependents. The balance in your LSA is the total amount available for you and all your dependents (not the amount available for each person). There’s nothing special you need to do when submitting a claim for a dependent’s expense, just submit as you normally would!